Popular Keywords

News

LEDinside:Weaker LED Demands Drives Down Sapphire Prices More than 30% YoY

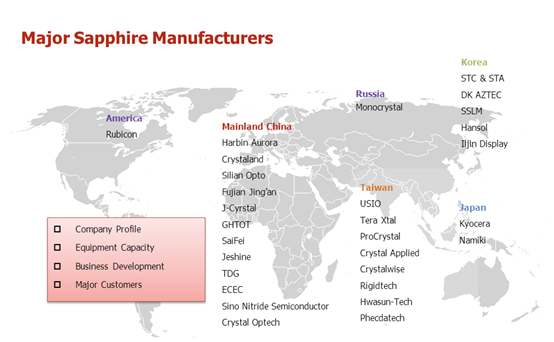

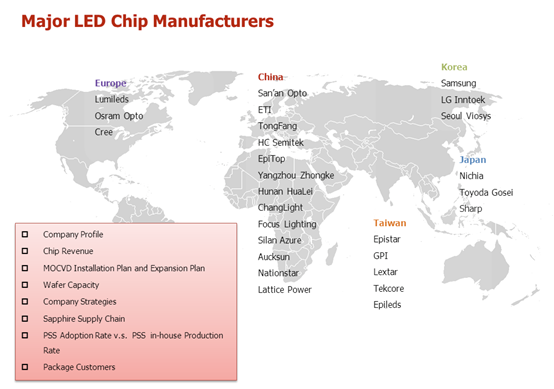

While prices are continuing their slide in the 6-inch sapphire market, a general increase in the 6-inch LED wafer yield rates may help generate demand. If the 6-inch LED wafer process had the same yield rate as the 2-inch, it could reduce the cost per unit by 69% because of advantages such as greater wafer surface for epitaxy and increased edge utilization rate. Thus, raising the yield rate on the 6-inch LED wafer process will expand the market demand for sapphire and effectively lower the inventory level. However, migrating to the 6-inch process is also a huge investment involving buying new equipment and overcoming technical hurdles in the backend chip manufacturing process. Transitioning from the 2-inch wafer production to the 4-inch is therefore much more cost effective right now than moving to the 6-inch. Raising the 6-inch LED wafer yield rate will depend on the technological capability of industry participants. LED chip manufacturers that are presently investing the 6-inch wafer production include Lumileds, Osram Opto, LG Innotek, Epistar, Nichia, Toyoda Gosei and Sharp. Chinese companies such as San’an Opto and Elec-Tech are also doing pilot runs on their 6-inch wafer production.

|

|