Popular Keywords

News

LEDinside Says Global UV LED Market to Expand at a CAGR of 34% From 2015 to 2020 as Applications for Related Solutions Emerge

Taiwan’s major annual optoelectronics industry exhibition, Photonics Festival 2017, will be held in Nangang Exhibition Hall of Taipei World Trade Center from June 14 to 16. Some of the highlights in the LED section of this exhibition includes products for the automotive industry and applications related to ultraviolet (UV) LEDs. LEDinside, a division of TrendForce, projects that the scale of the global UV LED market will increase from US$288 million in 2017 to US$526 million in 2020. Furthermore, the CAGR of the UV LED market in the 2015~2020 period is currently estimated at 34%. These and other data can be found in LEDinside’s 2017 UV LED vs. UV LED Module Market Report.

Uses of invisible LEDs have expanded in scope, creating new opportunities for the whole LED industry. At the same time, an increasing number of UV LED products have become available for curing, printing, exposure and other major applications. Demand for UV LEDs are expected to keep climbing as most countries worldwide have endorsed energy saving policies and ratified the Minamata Convention on Mercury.

“The largest source of revenue for UV LED suppliers in 2016 was the sales of UV-A LEDs,” noted Joanne Wu, research manager of LEDinside. “Because UV-A LEDs are mainly used for curing, some UV LED suppliers have entered the curing module market to further increase their profitability in this business.”

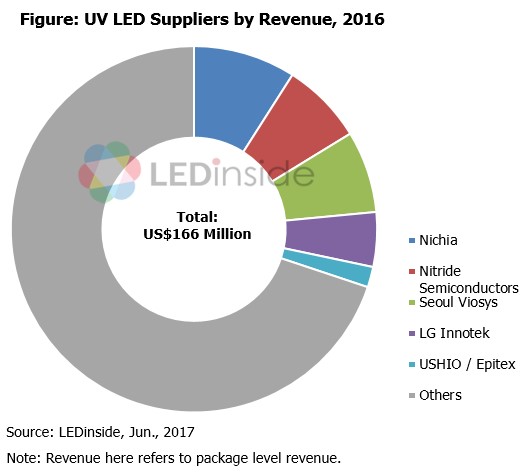

LED companies from South Korea and Japan were the dominant UV LED package suppliers by revenue in 2016. In the ranking, the top five suppliers in order were Nichia, Nitride Semiconductors, Seoul Viosys, LG Innotek and USHIO/Epitex. This year, South Korean LED companies are going to launch new series of UV-C LED products. UV-C LEDs, which have been technologically challenging to manufacture, will contribute greatly to South Korean suppliers’ revenues. Thus, there could be changes to this year’s revenue ranking.

Taiwanese LED companies are also eager to move away from the highly competitive blue LED market and into the UV LED market that has higher growth potential. Lextar, for instance, has released UV LEDs for curing and printing applications. The company is expected to accelerate product development and grow its client base this year. Likewise, LED chip maker High Power Lighting (HPL) and package supplier Epileds have formed a joint venture company Bioraytron that sells branded UV-C LED products. Bioraytron will also roll out new UV-C LED products in the second half of this year, and HPL anticipates that 30% of its annual revenue for 2017 will come from UV LEDs.

|

Looking at demand by applications, the largest segment of demand for UV-A LEDs comes from curing. Other major applications include printing and exposure. UV printing systems need LED modules that can produce a high level of irradiance, while UV exposure machines require LED modules that can achieve a high level collimated light. In addition, UV LEDs are also being deployed in some special curing applications that have recently emerged in the market.

As for UV-LEDs, recent technological advances in their manufacturing have allowed them to be deployed in more applications. LEDinside expects LED companies will roll out new UV-C products this year. Solutions for consumer appliances, air conditioners, air purifiers and still water purifiers will be first to arrive on the market and take off. UV-C LED products for flowing water purification are expected to enter the market later at a more opportune time.

- Why is UV LED Getting Popular?

- Wavelength and Applications

- UV LED Market Map

- Five Major UV Market Applications

- UV Market Applications

- 2016-2020 UV LED Market Scale

- 2016-2020 UV LED Market Scale By Applications

- 2016-2017 (F) Top 10 UV LED Revenue Ranking

- 2014-2016 UV LED Market Price Survey and Future Price Drop Forecast

- UV LED Market Opportunities and Challenges

- UV LED Market Value Chain Analysis

- 2018- 2020 UV LED Market Value Chain Analysis

- UV-A LED Package Types and Market Applications

- UV-A LED Products Enters High Price-Performance Ratio Era

- UV-A LED Product Specification and Application Requirement

- UV-A LED Player Progress

- UV Curing

- UV Technology Requirements in Curing Application Markets

- UV Curing Conditions

- UV Wavelength Distribution and Optical Design

- UV Irradiance vs. Radiant Energy Density

- UV Resin and Photoinitiator

- Free Radical Polymerization Curing

- Thickness and Energy

- Cooling System

- UV LED Penetration Rate Analysis- By Curing Application

- Curing Application Market Opportunity- By Region

- Curing Application Market Overview

- UV Curing Market Key Factors

- Curing Application Market Challenge- Optical Design

- Curing Application Market Challenge- Optical Design- Irradiance v.s. Irradiance Energy

- Curing Application Market Challenge- UV Adhesive- Customized Effect

- Curing Application Market Challenge- UV Adhesive- Oxygen Inhibition

- General Curing Market v.s. Exposure Machine Curing Market

- Traditional Printing and Digital Printing Analysis

- Printing Application Market Opportunity- By Technology

- 2010-2020 Printing Market Trend- By Application

- 2010-2020 Printing Market Trend- By Region

- UV LED Penetration Rate Analysis in Printing Market

- UV LED in Digital Printing Market- Possibilities and Challenges

- UV LED in Sheetfed Offset Market- Possibilities and Challenges

- 2016-2017 UV LED Module Market Size For Sheetfed Offset- Equipment Revenue and Major Companies' Revenue

- 2016-2017 UV LED Module Market Size For Sheetfed Offset

- UV LED Curing Process

- Printing Application Market Requirement

- Exposure Process

- UV LED in Exposure Machine Market

- Optical Design in Exposure Machine Market

- PCB / LCD Exposure Machine Market Demand and Major Players

- 2016-2020 UV LED Modules Market Size For PCB/ LCD Exposure

- Exposure Machine Market Requirement

- General Curing Market v.s. Exposure Machine Curing Market

- UV LED Nail Curing Application Market

- Nail Curing Manufacturer List

- Photocatalysis Combining with UV LED and TiO2 Coating

- Air Purifier Manufacturer List

- Manufacturer Development

- Product Features

- Future Plan

- Manufacturer Development

- Product Features

- Future Plan

- UV-C LED Product and System Requirements

- AlN / AlGaN on Sapphire’s Pros and Cons

- Bulk AlN / AlGaN’s Pros and Cons

- UV-C LED Technology Requirement

- UV-C LED Chip Technology

- UV-C Top Three Issue to Improve EQE

- UV-C LED Chip Technology Results

- UV LED Technology Evaluation

- UV-C LED Package Limitations and Technology Requirements

- UV-C LED Manufacturer Technology Trend

- UV-C Sterilization Principles

- Lethal Dose of UV-C on Various Bacteria and Viruses

- Sterilizing Effect of Irradiance for Microorganisms

- WHO Approved Irradiation Energy in Bacteria and Viruses

- Traditional UV-C Mercury Lamp and UV-C LED Tube

- UV-C LED Market Opportunity- Global Sterilization Market

- UV-C LED Market Opportunity

- Water: Drinking Water Purifier Manufacturer List

- Air: Air Purifier Manufacturer List

- UV-C Market Application and Requirement

- Water: UV Irradiation Device- Flow Style

- Water: Drinking Water Purifier Manufacturer List

- Food: Refrigerator Brand List

- Medical Treatment: Disinfection Market and Cancer Treatment

- Manufacturer Development

- Product Features

- Future Plan

+886-2-8978-6488 ext. 912