Popular Keywords

Articles

News

[News] Heated Competition Driven by the Booming AI Market: A Quick Glance at HBM Giants’ Latest Moves, and What’s Next

To capture the booming demand of AI processors, memory heavyweights have been aggressively expanding HBM (High Bandwidth Memory) capacity, as well as striving to improve its yield and competitiveness. The latest development would be Micron's reported new plant in Hiroshima Prefecture, Japan. The ...

News

[News] Taiwan Ministry of Economic Affairs Reportedly Eyeing on Establishing a Semiconductor Park in Kyushu

On May 30th, Taiwanese Minister of Ministry of Economic Affairs, J.W. Kuo, proposed a crucial industry policy. According to a report from China Times, the first step is to take Taiwan’s manufacturing parks global, with the initial site planned for Kyushu, in conjunction with TSMC's Kumamoto fab, ...

News

[News] EU Reportedly Delays Decision on Imposing Tariffs on Chinese Electric Cars

The European Commission initiated an investigation into Chinese electric cars in October last year, targeting BYD, SAIC Group and Geely, with plans to impose provisional tariffs on new electric cars imported from China. According to previous media reports, the plans were originally scheduled to be a...

News

[News] UMC Optimistic About Second Half Business Outlook, While AI Could Capture 10-20% Market Share

According to a report from Liberty Times, Taiwanese foundry UMC stated yesterday that the company’s operations in the second quarter would see a slight increase compared to the first quarter, and the second half of the year would be better than the first half. With UMC’s technology and proces...

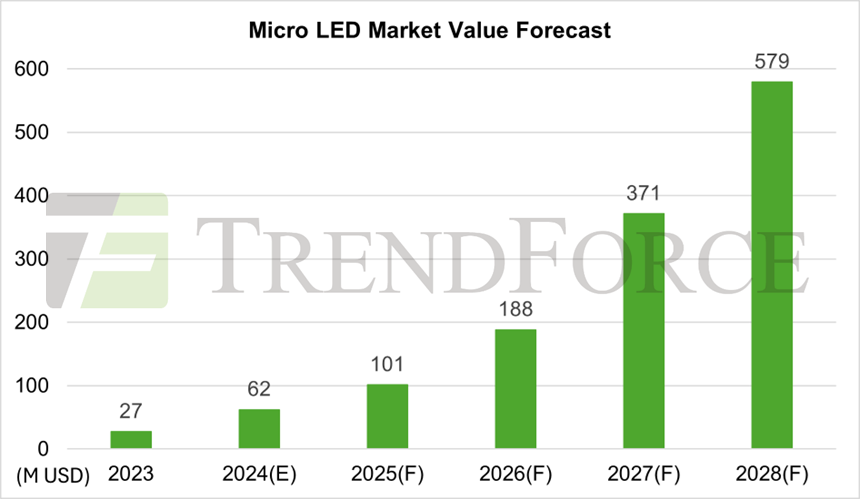

TrendForce:Head-mounted and Automotive Sectors Will Be the Focus for Micro LED Applications

The Micro LED development was hit hard in March 2024 after Apple decided to cancel the Micro LED watch project. Slowdowns in aspects including investments, technological development, and widespread use are unavoidable. Nevertheless, chip miniaturization, which is closely associated with cost reducti...

- Page 213

- 591 page(s)

- 2955 result(s)