Popular Keywords

Articles

News

[News] Continuous Breakthroughs in SiC Substrates, Global 8-Inch Fab to Reach 11

In recent years, with the continuous surge in demand for Silicon Carbide (SiC) substrates, the call for cost reduction in SiC has been growing stronger, as the ultimate product price remains the key determinant for consumers. The cost of SiC substrates accounts for the highest proportion in the enti...

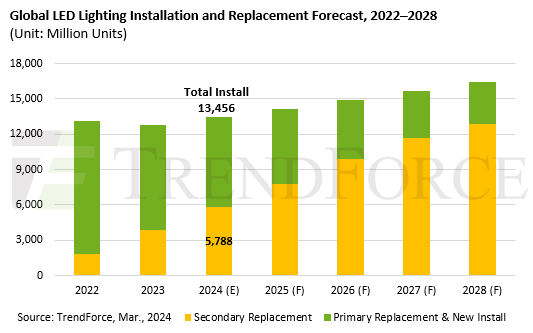

Global LED Lighting Industry Set to Benefit from an Estimated 5.8 Billion Units of Secondary Replacement Demand for LED Lamps and Luminaires in 2024, Says TrendForce

Mar. 4, 2024 ---- TrendForce’s latest reports indicate a significant turning point for the LED lighting market in 2024, as an estimated quantity of 5.8 billion LED lamps and luminaires reach the end of their lifespan. This milestone is set to trigger a substantial wave of secondary replacement...

News

[News] Intel Submits Conceptual Drawings for Fab Construction in Germany, Installing High-NA EUV Exposure Machines

In June 2023, leading processor manufacturer Intel reached an agreement with the German federal government, announcing the signing of an amended investment memorandum. The plan involves investing over EUR 30 billion to construct two new fabs in Magdeburg. The German federal government has agreed to ...

News

[News] Dell Leak Reveals NVIDIA’s Potential B200 Launch Next Year

NVIDIA has yet to officially announce the exact release dates for its next-generation AI chip architectures, the Blackwell GPU, and the B100 chip. However, Dell's Chief Operating Officer, Jeff Clarke, recently revealed ahead of schedule during Dell's Q4 2024 Earnings Call that NVIDIA is set to intro...

News

[News] NVIDIA Reportedly Overwhelms TSMC with 3 and 4-Nanometer Orders

The annual AI event, NVIDIA GTC (GPU Technology Conference), is set to take place on March 17th, as H200 and the next-generation B100 will reportedly be announced ahead of schedule to seize the market. According to Commercial Times’ report citing sources, H200 and the upcoming B100 will adopt TSMC...

- Page 269

- 585 page(s)

- 2922 result(s)