Popular Keywords

Articles

News

[New] The Reality of Micro LED Unveiled – Infinite Opportunities, Yet Initial Capacity Demand Remains Low

Ennostar, a Taiwanese group focusing on the R&D and manufacturing of Micro LED, LED and compound semiconductor, has announced on January 19th a NTD 670 million (roughly USD 21.36 million) sale of the planned Micro LED production facility in Zhunan, Taiwan. Its subsidiary, EPISTAR, is anticip...

News

[News] Subsidies from the U.S. Legislation “NAPMP” Potentially Expected to Cover IC Substrates

The U.S. Department of Commerce has initiated the "National Advanced Packaging Manufacturing Program (NAPMP) ," with materials and substrates being the first subsidized areas. Due to the close collaboration between IC testing and IC substrates, it is not ruled out that the IC substrate industry coul...

News

[News] China’s Chip Equipment Imports Surge 14% to Nearly USD 40 Billion in 2023

As companies increased their investments in 2023, the Chinese semiconductor industry actively expanded, leading to a substantial increase in the import volume of China's chip manufacturing equipment. According to Bloomberg’s report citing official Chinese customs data, the import value of equip...

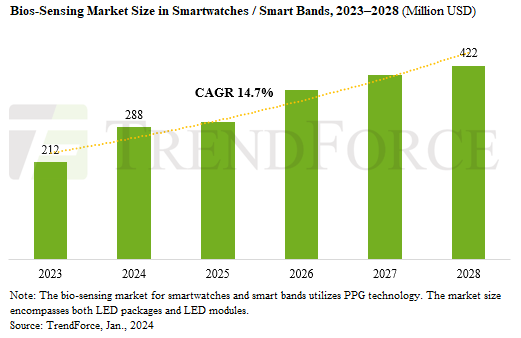

Benefited from Enhancing Bio-Sensing Technology, the Market in Wearable Device Applications to Reach US$422 Million, Says TrendForce

Jan. 22, 2024 ---- In a pivotal ruling, the U.S. Court of Appeals for the Federal Circuit has decided against Apple in its patent dispute with Masimo, mandating a halt in sales of the Series 9 and Ultra 2 in the US due to their blood oxygen features. This decision pushes Apple to potentially remove ...

News

[News] Expert Insights on NVIDIA’s AI Chip Strategy – Downgraded Version Targeted for China, High-End Versions Aimed Overseas

NVIDIA CEO Jensen Huang has reportedly gone to Taiwan once again, with reports suggesting a recent visit to China. Industry sources believe NVIDIA is planning to introduce downgraded AI chips to bypass U.S. restrictions on exporting high-end chips to China. Huang's visit to China is seen as an effo...

- Page 290

- 586 page(s)

- 2928 result(s)