Popular Keywords

Articles

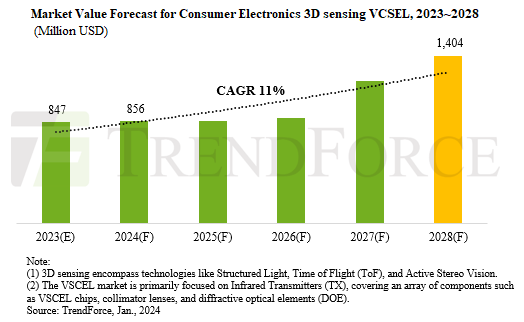

Market Value of Consumer Electronics 3D Sensing VCSEL Forecast to Soar to US$1.404 Billion by 2028, Says TrendForce

Jan. 10, 2024 ---- TrendForce’s latest report, “TrendForce 2024 Infrared Sensing Application Market and Branding Strategies” reveals a market decline for consumer electronics 3D sensing VCSEL in 2023 to US$847 million. This downturn has been attributed to a weak consumer market and...

News

[News] Explore the Foundry Landscape in Singapore as UMC’s Plant Nears Completion Mid-Year

Recent reports have suggested that UMC's new facility in Singapore is set to be completed by mid-2024, with initial production expected to commence in early 2025. UMC has announced that, in response to the demand for capacity expansion, the board of directors has approved a capital expenditure ex...

News

[News] Microchip’s Disappointing Financial Report Raises Caution in the Semiconductor Industry

On January 8th, leading U.S. microcontroller (MCU) and analog IC manufacturer Microchip raised concerns, stating that the revenue for the last quarter would experience a more significant decline than previously estimated, falling short of overall expectations. The market perceives Microchip's fin...

Insights

[Insights] Light Trading, Stable DRAM and NAND Flash Spot Prices

Based on TrendForce's weekly memory spot price trends released every Wednesday, due to the year-end holiday period, the spot market for DRAM and NAND Flash experiences light trading, and prices remain relatively stable. For details, please refer to the information below: DRAM Spot Market: Due ...

News

[News] SK Hynix Aims for Doubling Market Value in 3 Years, Considering Alteration On its Production Cut Plan for Q1

SK Hynix CEO Kwak Noh-Jung expressed optimism at the Consumer Electronics Show (CES) in the United States, stating that artificial intelligence (AI) chips would propel SK Hynix's market value to double within three years, reaching KRW 200 trillion (approximately USD 152 billion). Kwak also reveal...

- Page 298

- 587 page(s)

- 2932 result(s)