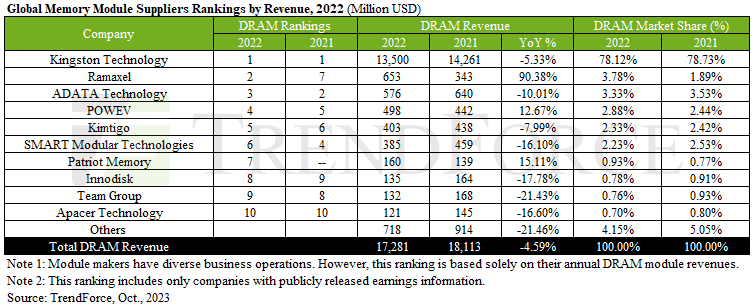

TrendForce reports that consumer appetite for electronic products took a hit from high inflation, with global DRAM module sales in 2022 reaching US$17.3 billion—a 4.6% YoY decline. Revenue performance varied significantly among module makers due to the different domains they supply.

TrendForce’s data indicated that the top five memory suppliers in 2022 accounted for 90% of total sales, with the top ten collectively capturing 96% of global market revenue. Kingston maintained its dominant market share of 78%. Even with a slight revenue dip, it held steadfast to its position as the global leader. Despite poor end-market demand, Kingston’s robust brand scale, along with its comprehensive product supply chain, limited its revenue decline to a modest 5.3%, keeping it firmly at the top of market share rankings.

Revenue performances diverged among module manufacturers due to different brand strategies

Raxamel, ranking second, pulled off an impressive feat by experiencing nearly 90% growth in 2022. However, a deeper look reveals that this surge is largely attributed to a significant decline in 2021, creating a low comparison base. Excluding 2021, its revenue trends reasonably when compared with previous years. Ramaxel achieved substantial gains in the server domain last year and received validation from server OEM clients, also exhibiting steady supply growth in the PC OEM segment. These factors contributed to its revenue growth in 2022, aligning with the company’s operational achievements.

ADATA—focusing mainly on consumer products—also ventured into high-margin products in industrial control, automotive, and e-sports last year, but their current low proportion made it hard to withstand the impacts of global demand shrinkage, leading to a 10% revenue decline and third place.

POWEV, buoyed by its brand's success in the e-sports market and a diverse channel sales model, saw its revenue grow by 12.7%, landing it the fourth spot. Despite Kimtigo's proactive product development and global expansion, it couldn't overcome the slide in consumer electronics spending, resulting in a revenue decline, and its revenue ranking slightly rose to fifth in 2022.

SMART Modular, primarily serving the industrial control market, faced challenges due to inflation, leading to constrained corporate procurement budgets and decreased demand. Consequently, its revenue fell by 16.1%, placing it sixth. Patriot Memory, making a comeback on the list, aggressively expanded new ventures and responded to national project demands in 2022, pushing its revenue up by 15.1% and achieving the seventh rank.

Revenue contributions remain limited in the early growth stages of new applications; revenues plunge by over 15% amid the global economic downturn

Innodisk, advancing from ninth to eighth, relied on its strong foundation in industrial application development, extending its efforts to industrial AIoT-related applications. Yet, as this field is still nascent, it struggled against the downward trend in demand for its core industrial control products, leading to a 17.8% fall in revenue.

Team Group was impacted by channel inventory depletion in 2H22 and witnessed a stark demand decrease and a 21.4% annual revenue reduction, dropping it to ninth place. However, the active promotion of its e-sports brand targeting niche markets suggests potential revenue growth if computer-related demands rebound. Apacer, positioned at tenth, faced the global economic slump, with weakening end-sale forces in the latter half of 2022 and more conservative customer orders, resulting in a 16.6% revenue downturn.

For more information on reports and market data from TrendForce’s Department of Semiconductor Research, please click here, or email the Sales Department at SR_MI@trendforce.com

For additional insights from TrendForce analysts on the latest tech industry news, trends, and forecasts, please visit at https://www.trendforce.com/news/

Subject

Related Articles

Related Reports